By Alex Whalen

and Tegan Hill

The Fraser Institute

Due largely to COVID-19, the big banks project negative growth for Nova Scotia’s economy in 2020, ranging from –5.5 per cent to –7.4 per cent.

Without a strong rebound, such a steep recession could have a lasting impact on living standards in the province and Maritime region more broadly. And those living standards are already well below the Canadian average.

To help support a strong recovery, the provincial government of Premier Stephen McNeil should address policy problems that existed before the recession, including Nova Scotia’s high personal income tax rates.

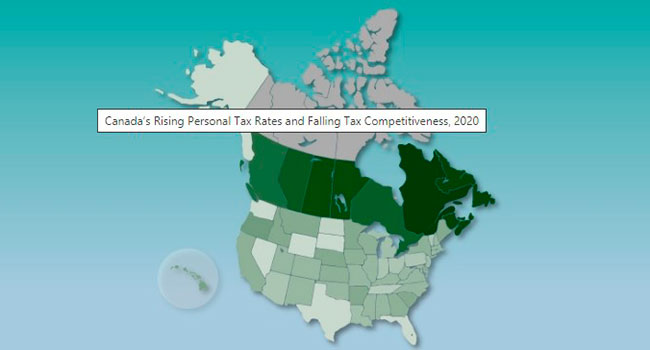

A recent study found that out of 61 jurisdictions in Canada and the United States, Nova Scotia has the highest top combined (federal/provincial or federal/state) personal income tax rate (54 per cent), highest rate at $150,000 in income, third-highest rate at $75,000 in income and second-highest rate at $50,000 in income.

How did this happen?

In 2010, Nova Scotia added a new higher top personal income tax rate, which targets entrepreneurs, doctors and other skilled professionals. To make matters worse, in 2016 the federal government increased the top federal personal tax rate from 29 per cent to 33 per cent.

As a result of these changes, Nova Scotia’s top combined rate has increased by 5.8 percentage points since 2009.

At the same time, federal tax reform in the U.S. lowered the top federal rate by 2.6 percentage points, from 39.6 per cent to 37 per cent. So as Nova Scotia’s rates were rising, competitors south of the border have enjoyed federal tax relief.

Of course, tax policy decisions must be made in light of Nova Scotia’s large budget deficit and mounting government debt.

However, attempting to fight these deficits while maintaining high personal income tax rates will reduce the province’s economic growth prospects, with negative implications for job creation and income growth. That’s because high marginal income tax rates discourage work, savings and investment. Empirical evidence suggests there’s substantial economic harm associated with each dollar raised by higher income tax rates.

Moreover, high income tax rates can influence people’s decisions on where to work or start new businesses. All else equal, jurisdictions with higher income tax rates are less likely to attract mobile professionals and entrepreneurs, the lifeblood of any economy, than jurisdictions with lower rates.

Consider a skilled professional with a high income, or a promising entrepreneur with a strong business plan, deciding where to live. She could choose Nova Scotia and face a top combined rate of 54 per cent or somewhere in the U.S. and find a top marginal rate as low as 37 per cent.

Of course, individuals consider a wide range of factors when deciding where to live (and potentially work, invest and create jobs), but the difference in personal income taxes can play a role in that decision.

As the economy emerges from COVID-19, provinces must look for ways to support recovery and prosperity. Reducing uncompetitive personal income tax rates in Nova Scotia would help create a pro-growth tax policy environment.

And that would boost the province’s prospects for a strong economic rebound and future prosperity for Nova Scotians and their families.

Tegan Hill and Alex Whalen are policy analysts at the Fraser Institute. This op-ed was co-authored by Ben Eisen, a Fraser Institute analyst.

Tegan and Alex are Troy Media Thought Leaders. Why aren’t you?

![]()

The views, opinions and positions expressed by columnists and contributors are the author’s alone. They do not inherently or expressly reflect the views, opinions and/or positions of our publication.